THE THE BOSTON CONSULTING GROUP BOSTON CONSULTING GROUP UNIVERSITÀ UNIVERSITÀ DI DI GENOVA GENOVA Corso di Laurea in Ingegneria Gestionale Corso di Laurea in Ingegneria Gestionale 31 Gennaio 2003 31 Gennaio 2003

Transcript

THE THE BOSTON CONSULTING GROUPBOSTON CONSULTING GROUPUNIVERSITÀUNIVERSITÀ DI DI GENOVAGENOVA

Corso di Laurea in Ingegneria GestionaleCorso di Laurea in Ingegneria Gestionale

31 Gennaio 200331 Gennaio 2003

Experience curve e la Experience curve e la matrice BCGmatrice BCG

-2-UniGenova-January2003

PORTFOLIO MATRIX IS A TOOL ORIGINALLY DEVELOPED TO ASSESS CASH FLOWS BALANCE WITHIN A FIRM

Business portfolio of group xxx, B ITL 1996

Why growth is a proxy for cash absorbed? Why market share is a proxy for cash generated?

• What impacts cost, in particular?

Why growth is a proxy for cash absorbed? Why market share is a proxy for cash generated?

• What impacts cost, in particular?

1%

10%

10 1 0.1 0.01

ConsumerProducts

OTCdrugs

RX drugs

Wholesaling

Seeds

Wines

Packed meat

Industrial machines

Market growth

Relative market share

Star Questionmark

Cash cow Dog

5%

Fatt. 100 Mdi

Business controllatiBusiness in JV

cashabsorbed

cashabsorbed

cashgenerated

cashgenerated

-3-UniGenova-January2003

SCALE, EXPERIENCE, COMPLEXITY, AND UTILIZATIONHAVE DISTINCT COST EFFECTS

Scale• Relates unit cost or price to production volume• Generally applies to machines or facilities of different sizes at a point in time

Experience• Relates unit cost or price to cumulative production• Best to think in terms of entire industry experience over long periods• Arises for a variety of economic reasons• Is used a lot less frequently than you may think

Complexity• Relates unit cost to some measure of complexity• Either

- over time- over different facilities at a point in time

Utilization• Relates unit cost or profitability to utilization as a percentage of capacity• Applies to different volumes or output from given facilities over time

-4-UniGenova-January2003

SOMETIMES UNIT COSTS HAVE A “CONSTANT ELASTICITY”

y

x

log y

log x

Which examples follow this behaviour?• Under which circumstances?

Which examples follow this behaviour?• Under which circumstances?

-5-UniGenova-January2003

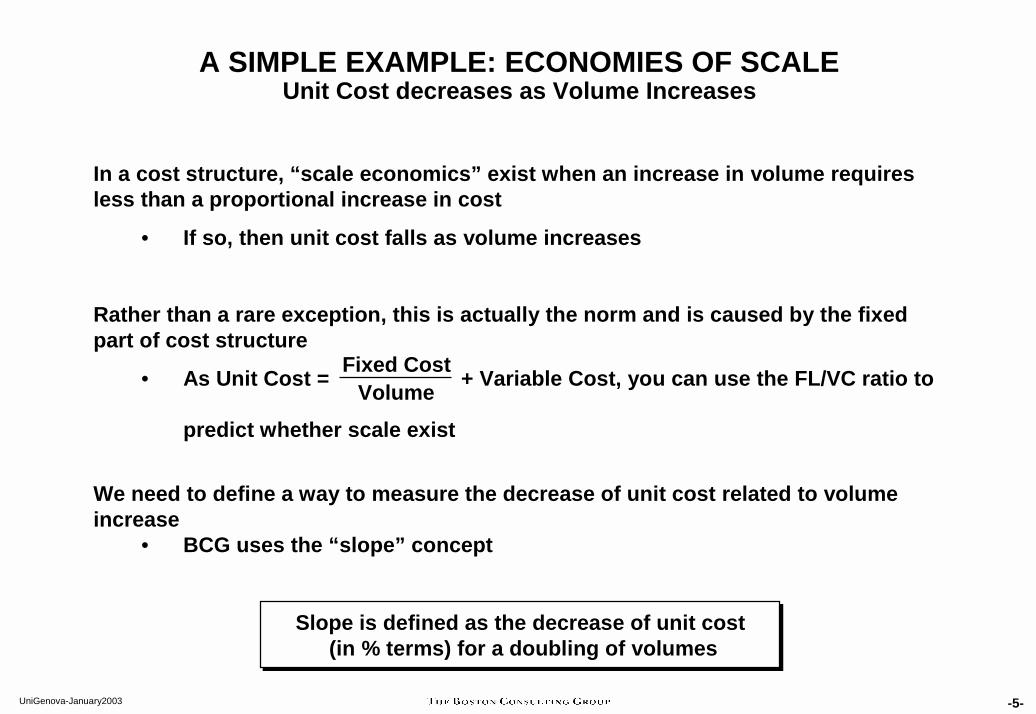

A SIMPLE EXAMPLE: ECONOMIES OF SCALEUnit Cost decreases as Volume Increases

In a cost structure, “scale economics” exist when an increase in volume requires less than a proportional increase in cost

• If so, then unit cost falls as volume increases

Rather than a rare exception, this is actually the norm and is caused by the fixed part of cost structure

• As Unit Cost = + Variable Cost, you can use the FL/VC ratio to

predict whether scale exist

We need to define a way to measure the decrease of unit cost related to volume increase

• BCG uses the “slope” concept

Volume

Slope is defined as the decrease of unit cost(in % terms) for a doubling of volumes

Slope is defined as the decrease of unit cost(in % terms) for a doubling of volumes

Fixed Cost

BCGBCG slopeslope

-7-UniGenova-January2003

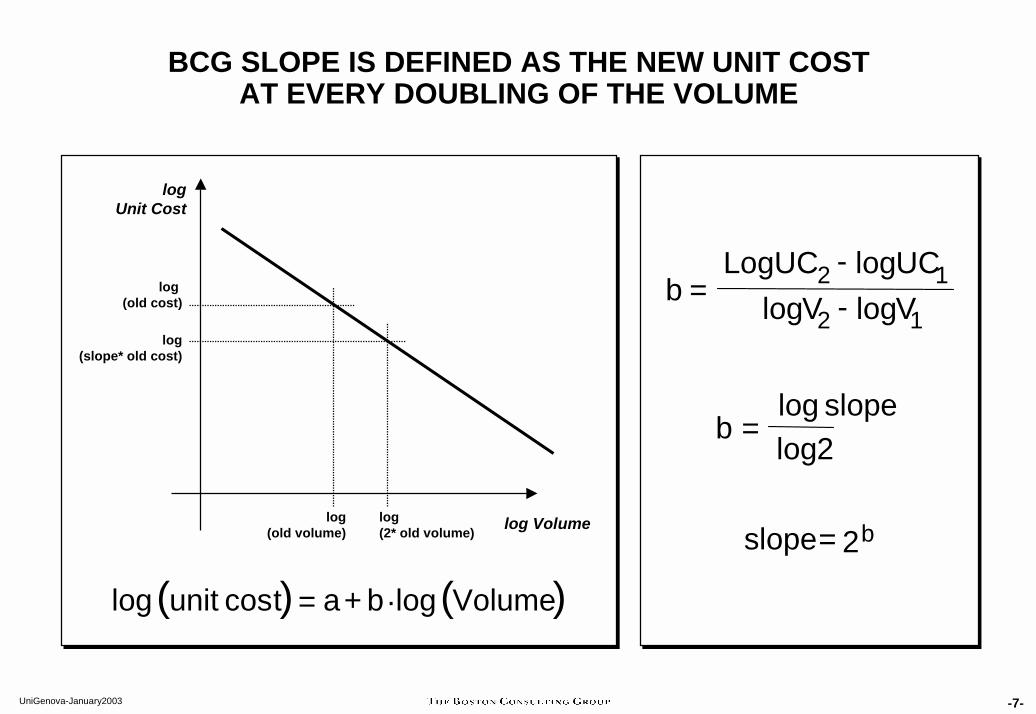

BCG SLOPE IS DEFINED AS THE NEW UNIT COSTAT EVERY DOUBLING OF THE VOLUME

( ) ( )Volumelogcoslog ·+= batunit

log Unit Cost

log Volumelog(old volume)

log(2* old volume)

log (old cost)

log (slope* old cost)

b2slope=

2log=log slope

b

12

12logloglog

--

= VVUCLogUC

b

-8-UniGenova-January2003

DIFFERENT COST SLOPES (LOG-LOG)YIELD DIFFERENT BCG SLOPES

InterpretationBCGSlope

100%

90%

80%

70%

60%

50%

50%

100%

s =

s >

s <

s =

s =

s =

s =

s =

Slope oflog V, log UC

0

-.152

0

-.322

-.515

-.737

-1

-1

b =

b >

b <

b =

b =

b =

b =

b =log V

Log UC

-9-UniGenova-January2003

TWO WAYS TO CALCULATE ECONOMIES OF SCALE (BCG SLOPE) Starting from observed data point

(1) Find approximate doubling of V to 2V (not log V, log 2V!)

(2) Calculate S

UC2 (at 2V)

UC1 (at V)

(3) If necessary derive b (not often)

log S

log 2

Easy method for quick estimate

Easy way: Derive S from doubling V Calculate b, then determine UC

b =

S =

(1) Convert V, UC to log V, log UC

(2) Determine slope b (of log V, log UC)

• For multiple data points, regress:

log UC = a + b log V

• For 2 data points, calculate slope:

b =

(3) Derive S from b, using:

S = 2b

Only method with regression

log UC2 – log UC1

log V2 – log V1

•

-10-UniGenova-January2003

TWO WAYS TO PREDICT UNIT COST IMPACT FROM SCALEStarting from BCG slope and starting / ending volumes

(1) If V doubled, predicted UC2 is simple:

UC2 = S UC1

(1) Derive b from S, using

b =

(2) Plug in b, old V1, UC1, new V2 (logs!)into slope equation;

b =

and solve for new log UC2

(3) Translate log UC2 out of log

UC2 = UC1

Easy way: Predict UC2 from doubling V Calculate b, then determine UC

log Slog 2

log UC2 – log UC1

log V2 – log V1

( (V2V1

b•

•

-11-UniGenova-January2003

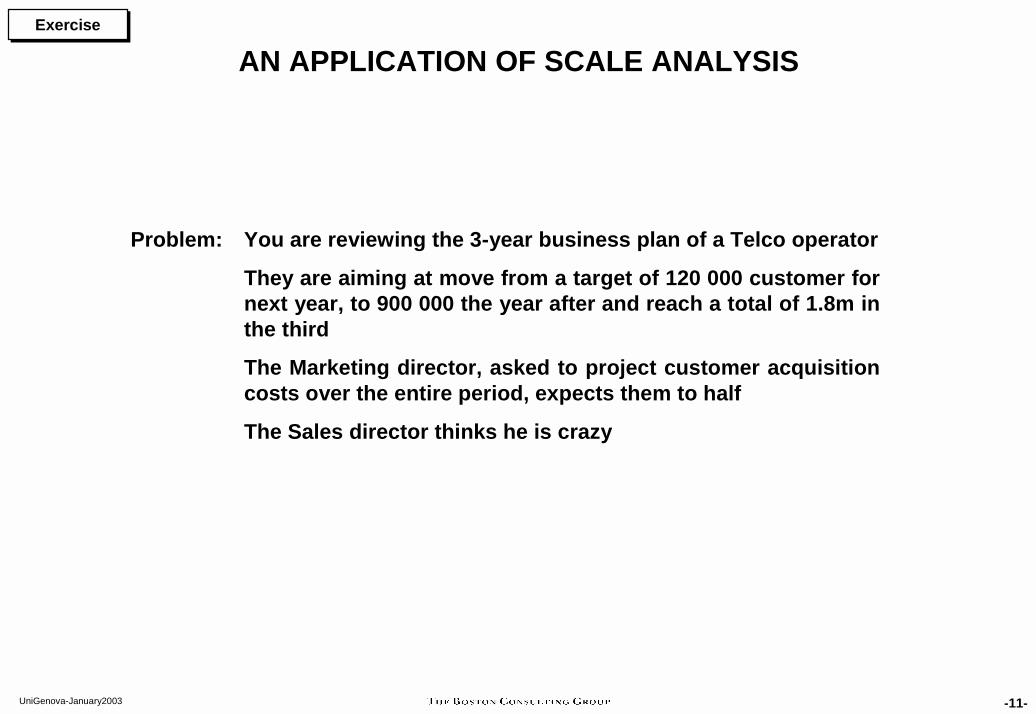

AN APPLICATION OF SCALE ANALYSIS

Problem: You are reviewing the 3-year business plan of a Telco operator

They are aiming at move from a target of 120 000 customer for next year, to 900 000 the year after and reach a total of 1.8m in the third

The Marketing director, asked to project customer acquisition costs over the entire period, expects them to half

The Sales director thinks he is crazy

ExerciseExercise

-12-UniGenova-January2003

ECONOMIES OF SCALE SIGNIFICANTLY REDUCE ACQUISITION AND RECURRING COSTS

Example: acquisition costs for a Telco operator, €/client

ExerciseExercise

10

42

32

Activation

Sales and distribution

Incentives

Marketing

70

90

87

?

?

X 2Clients (‘000) X 8116 1 856928

90

80

?

?

?

?

?

??

“Slope” (%)

?

Overall activity cost slope is … %

This information can support• Projection of future evolution

of cost, given expected volumes

• Estimate of cost position for competitors at different scale, given the cost of factors

• Simulation of impact of managerial options

- i.e. increase/reduce fixedvs variable selling cost

4

-13-UniGenova-January2003

WARNING: WHEN LOOKING FOR SCALE, LOOK THE RIGHT WAYFind the meaningful scale relation

Illustration: tissue manufacturing

No economies of scale ?No economies of scale ? Sure, but only by machine sizeSure, but only by machine size

•

•

•

•

•

•

P1

P2

P3

P6

P4

P5

Costper ton

($/t)

Plant size000 tonn/ year

Costper ton

($/t)

Machine size000 ton/ year

•

• •

••

•

P6

P1 P3

P4

P2

P5

Px : plant x

-14-UniGenova-January2003

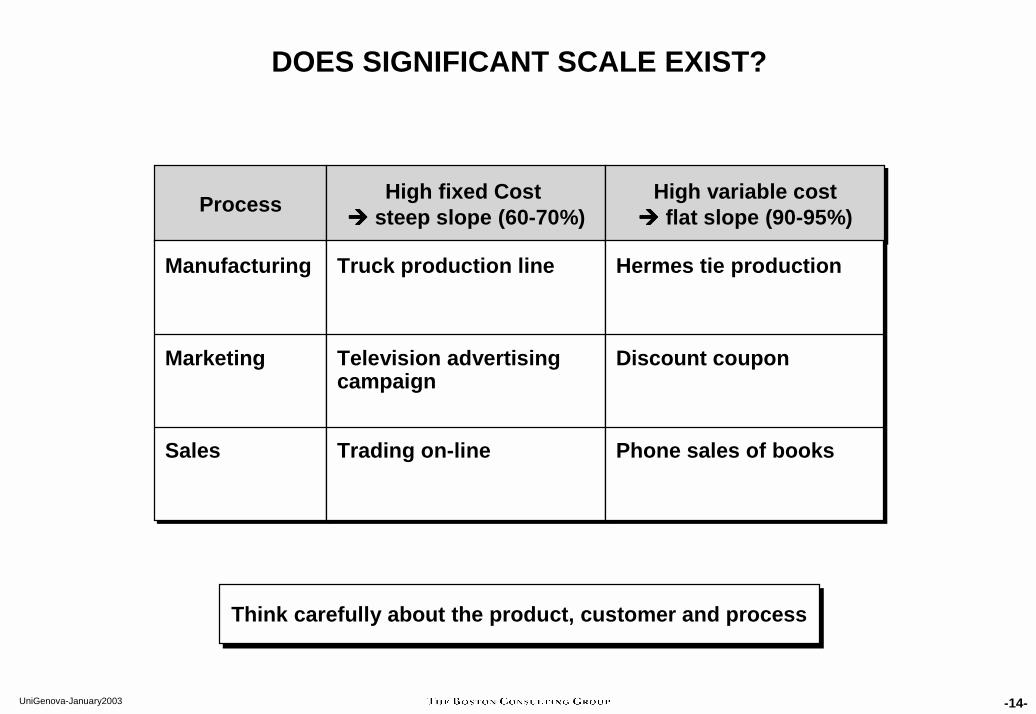

DOES SIGNIFICANT SCALE EXIST?

Think carefully about the product, customer and processThink carefully about the product, customer and process

ProcessProcess

Manufacturing

Marketing

Sales

Manufacturing

Marketing

Sales

High fixed Cost !!!! steep slope (60-70%)

High fixed Cost !!!! steep slope (60-70%)

Truck production line

Television advertising campaign

Trading on-line

Truck production line

Television advertising campaign

Trading on-line

High variable cost!!!! flat slope (90-95%)

High variable cost!!!! flat slope (90-95%)

Hermes tie production

Discount coupon

Phone sales of books

Hermes tie production

Discount coupon

Phone sales of books

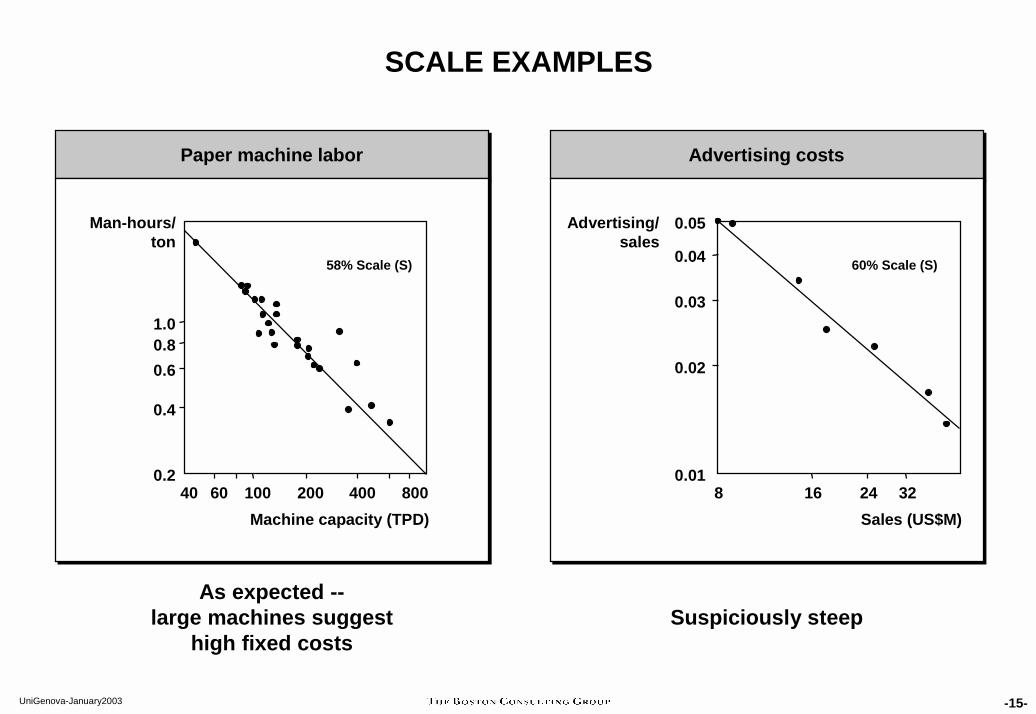

-15-UniGenova-January2003

SCALE EXAMPLES

Paper machine laborPaper machine labor Advertising costsAdvertising costs

Man-hours/ton

1.00.80.6

0.4

0.240 60 100 200 400 800

58% Scale (S)

Advertising/sales

0.05

0.04

0.03

0.02

0.018 16 24 32

Machine capacity (TPD) Sales (US$M)

As expected --large machines suggest

high fixed costsSuspiciously steep

60% Scale (S)

-16-UniGenova-January2003

HOWEVER, THINK BEYOND THE DATAFirst Cut of Data Would Show Wide Dispersion

Salaried andIndirect Employees/

Sales ($M)

10.0

5.0

3.0

2.0

1.0

0.52 5 10 20 50 100 200

100

30

Plant Sales/Product Family ($M)

Traditional ApproachCost-based Management ApproachTime-based Management Approach

70

Automotive Component Suppliers

Source: BCG Analysis

-17-UniGenova-January2003

DIFFERENT VOLUME LEVELS CAN JUSTIFYSUPERIOR TECHNOLOGIES

Conventional Lathes by Mechanical Design

MachiningCost/Piece

Manual Universal Machine

ManualCopy Lathe

ManualChucker

AutomaticSingle Spindle

AutomaticMultispindle

Lot Size

-18-UniGenova-January2003

NOT ONLY SCALE HAS AN IMPACT ON COSTS: EXPERIENCE CURVE (I)

Learning restricted within companies

Direct Cost/ MW

380

340

300

2605 15 50

Allis-Chalmers

Westinghouse General Electric

Firm Cumulative Megawatts (M)

Direct Costs Per Megawatt Steam Turbine Generators 1946-1963

-19-UniGenova-January2003

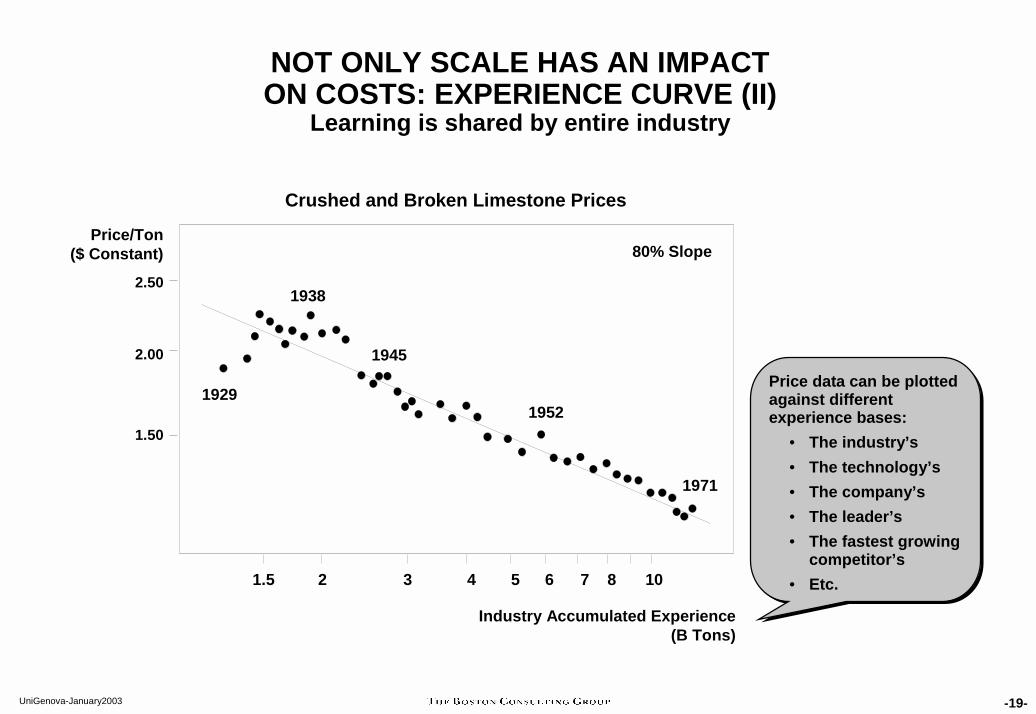

Crushed and Broken Limestone Prices

1.5 2 3 4 5 6 7 8 10

Industry Accumulated Experience (B Tons)

1929

1938

1945

1952

1971

80% Slope

2.50

2.00

1.50

Price/Ton($ Constant)

Price data can be plotted against different experience bases:

• The industry’s• The technology’s• The company’s• The leader’s• The fastest growing

competitor’s• Etc.

Price data can be plotted against different experience bases:

• The industry’s• The technology’s• The company’s• The leader’s• The fastest growing

competitor’s• Etc.

NOT ONLY SCALE HAS AN IMPACTON COSTS: EXPERIENCE CURVE (II)

Learning is shared by entire industry

-20-UniGenova-January2003

Complexity gives rise to unit costs that increase with the scope of activity

• Scope in manufacturing: parts, models, product lines, etc. . . .

• Scope in administration: businesses, countries, etc. . . .

• Complexity often works against scale

Example: the cost of connecting every two people in a communication network with a dedicated connection at $1 per connection

2 1 0.55 10 2

10 45 4.550 1,225 24.5

100 4,950 49.5

COMPLEXITY COSTS ARISE FROM PROBLEMSAND COSTS INVOLVED IN COORDINATING MANY ACTIVITIES

Number Number of Connections of People (~) [(N)(N-1)/2] Cost/Person ($)

-21-UniGenova-January2003

COMPLEXITY ARISES IN INDUSTRY DUE TO MANY FACTORS

Plant makes so many products that machines spend substantial time changing over between products

Salesmen sell too many products to master any one of them properly

Multiproduct plant has high administrative costs of coordination and tracking

-22-UniGenova-January2003

Machine ManufacturingMachine Manufacturing Other ManufacturingOther Manufacturing

COMPLEXITY EXAMPLES

Indirect Cost(% of Total

Cost)

139%

Indirect Cost(% of Total

Cost)

30

20

10

55 10 20 40

50

30

20

10

4 5 6 8 10 15 20 30 40 50# of Product Families Produced # of Models

8 Factories

Source: BCG Interviews and Analysis

-23-UniGenova-January2003

Health Care ServicesHealth Care Services Printing PressesPrinting Presses

Utilization is important when• Capital intensity is high• Energy consumption is major part of costs• Startup costs are high• Labor force is not flexible

Different from scale• Frequently the two phenomena interact

Utilization is important when• Capital intensity is high• Energy consumption is major part of costs• Startup costs are high• Labor force is not flexible

Different from scale• Frequently the two phenomena interact

Note: Assumes 2,000,000 Run Length

5

10

15

20

-24-UniGenova-January2003

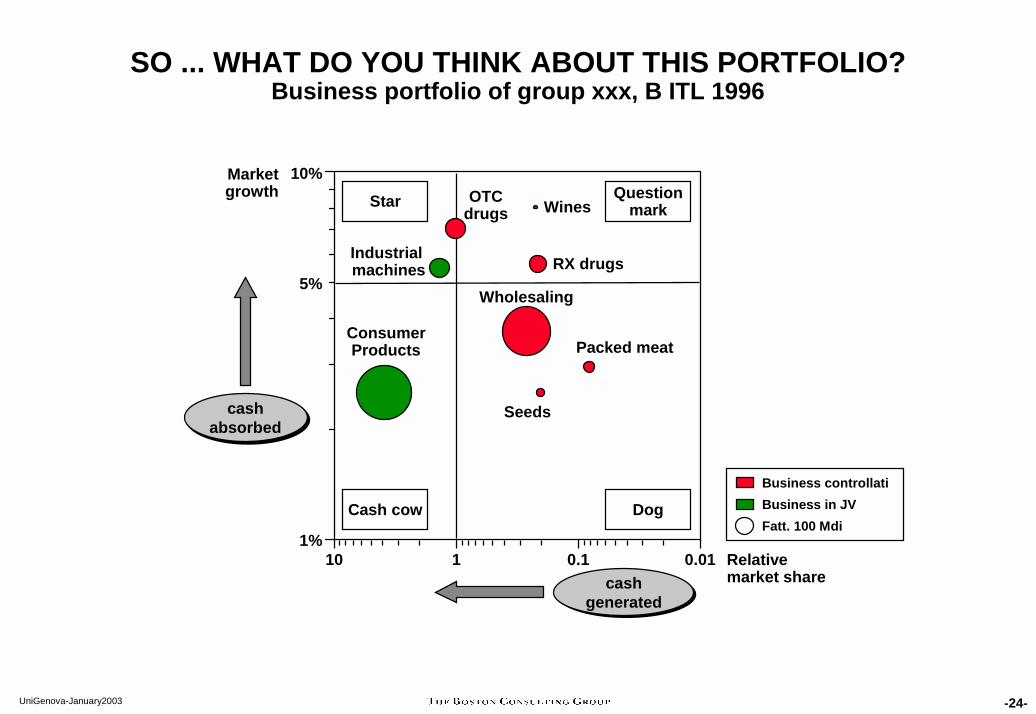

SO ... WHAT DO YOU THINK ABOUT THIS PORTFOLIO?Business portfolio of group xxx, B ITL 1996

1%

10%

10 1 0.1 0.01

ConsumerProducts

OTCdrugs

RX drugs

Wholesaling

Seeds

Wines

Packed meat

Industrial machines

Market growth

Relative market share

Star Questionmark

Cash cow Dog

5%

Fatt. 100 Mdi

Business controllatiBusiness in JV

cashabsorbed

cashabsorbed

cashgenerated

cashgenerated

-25-UniGenova-January2003

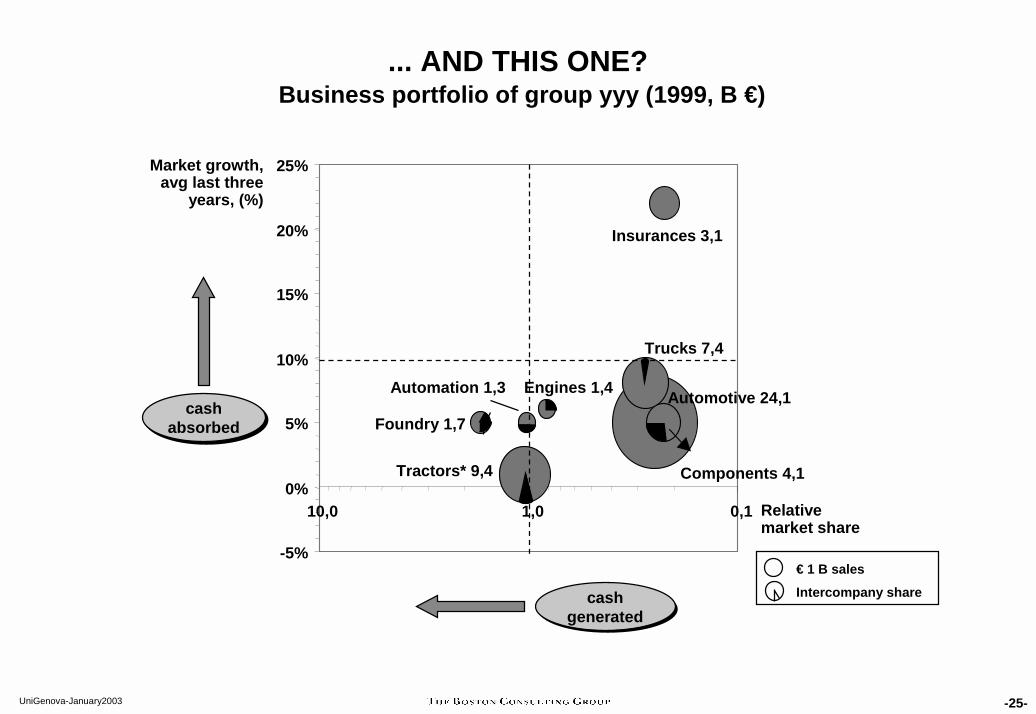

Automation 1,3

Tractors* 9,4

Insurances 3,1

Automotive 24,1Engines 1,4

Trucks 7,4

Foundry 1,7

Components 4,1

-5%

0%

5%

10%

15%

20%

25%

0,11,010,0

... AND THIS ONE?Business portfolio of group yyy (1999, B €)

Market growth, avg last three

years, (%)

€ 1 B salesIntercompany share

cashabsorbed

cashabsorbed

cashgenerated

cashgenerated

Relative market share

An An excerciseexcercise

-27-UniGenova-January2003

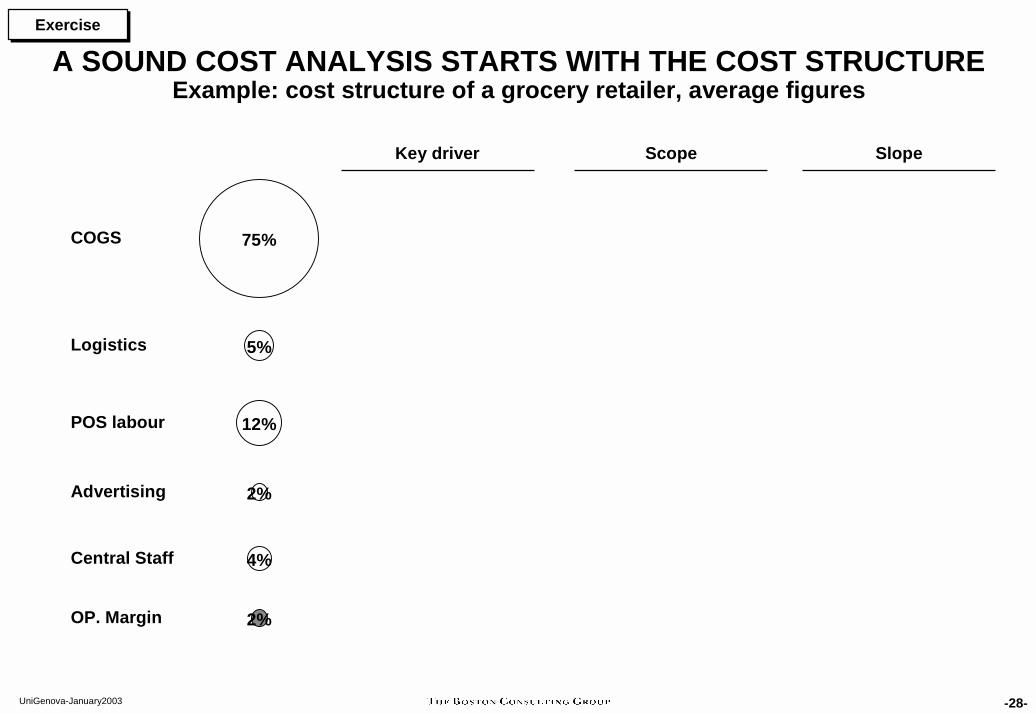

A SOUND COST ANALYSIS IS THE BASE FOR STRATEGIC DECISIONS

Problem: Sirio, a 1 bn € grocery retailer, with strongholds in 2 of the 8 regions of the country is overlooking 3 options for acquisition

• Andromeda, a same-sized national retailer

• Berenice, a 500m € local retailer competing in same regions

• Cassiopea, a 500m € local retailer competing in bordering regions

Which option would provide the highest competitive advantage from an operating cost perspective ?

ExerciseExercise

-28-UniGenova-January2003

A SOUND COST ANALYSIS STARTS WITH THE COST STRUCTUREExample: cost structure of a grocery retailer, average figures